Examples of behavioural economic policies include:

- Moving healthy food towards the check out or front area of the shop [In train stations in the Netherlands, this doubled sales of healthy food].

- Pension schemes in the UK for employed workers moved from opt in to opt out. So now, employees automatically enrol in their employers’ pension scheme. This led to 5.4 million more people saving via their workplace pension.

- Many countries have changed organ donation schemes from opt-out to opt-in, including the Netherlands.

- To encourage people to wash their hands for 20 seconds during the Covid-19 pandemic, UK officials suggested singing “happy birthday” while washing hands.

- Tax prompts, such as “most people pay their tax on time“, to encourage timely payment of taxes in the UK. Initial tests resulted in about £300 million of tax revenue being brought forward (as opposed to being paid late).

- Letters to doctors who were prescribing high amounts of antibiotics led to a 3.3% drop in prescriptions among this group.

Contents

Definitions

Choice architecture / framing – changing how a choice is presented to change how consumers react.

Default choice – this involves changing the default option. For example changing a process from opt-in (the default option is not to participate) to opt-out (the default option is to participate).

Restricted choice – reducing the number of choice options. This may help reduce consumer confusion, specifically “choice overload”. For example, restricting the number of plans that energy companies can offer consumers.

Mandated choice – legal consequences to a particular choice. Note this does not mean that either choice needs to be illegal. But choosing an action may legally prevent you from doing other things. For example to renew or apply for a driving licence online in the UK, you have to state whether you are willing to be an organ donor. In this case, if you don’t want to state whether you are willing to be an organ donor, there is a consequence: you cannot renew a driving licence online.

A nudge is a change to the choice architecture that does not restrict freedom to choose. But nudges can still alter people’s behaviour without changing incentives significantly.

Effects of nudges – positive externalities

There are nudges to encourage healthy eating to account for positive externalities in consumption.

In the case of health, it may be the case that consumers underestimate the long-term health benefits of healthy eating. This leads to underconsumption of healthy foods.

In the case of healthy food, there are positive externalities. A healthier workforce increases worker productivity, increasing wages, tax revenue. It reduces the burden on health care systems. This benefits taxpayers, government and firms. For example firms benefit from more productive workers, increasing their profits.

A nudge such as moving healthy options to the check out area for train stations in the Netherlands can increase healthy food demand. In this instance sales of healthy food doubled.

So demand shifts right from MPB to MSB. This increases the quantity of healthy food consumed from q to q1, so the quantity is now socially optimal, and the price increases from p to p1. This creates a welfare gain of area ABE.

Consumers may also have a default bias towards a particular type of food they are accustomed to eating.

Making consumers more likely to consume healthy food with this nudge can also interrupt this bias. This makes consumers more likely to develop new healthy eating habits.

Nudges to counter bias or improve information

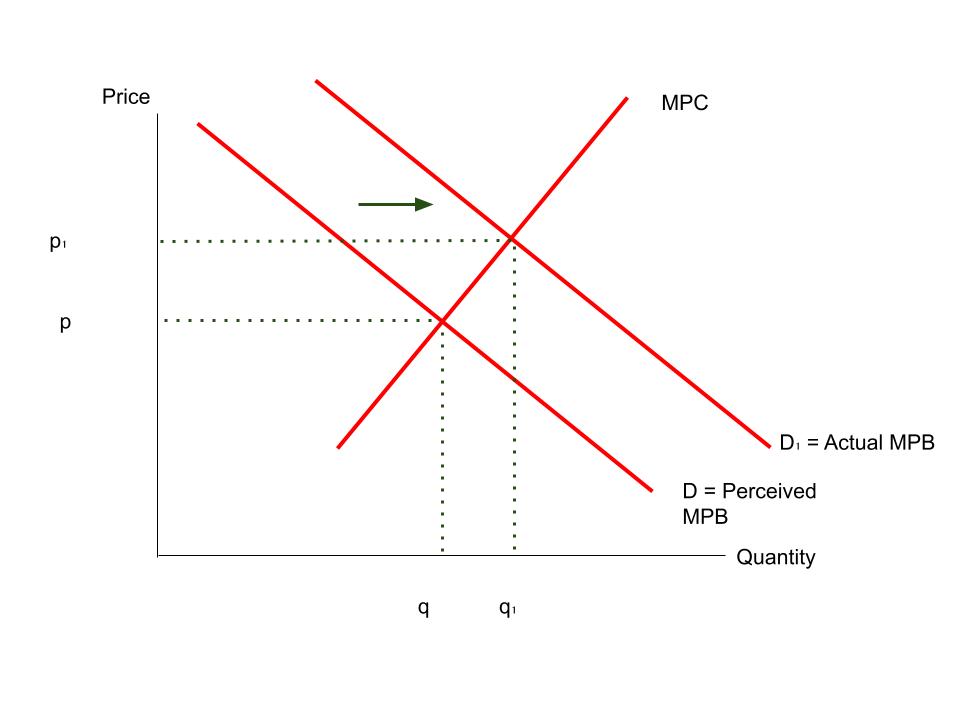

The UK Government has changed choice architecture around pensions.

Pensions are underprovided in the free market, because people may be myopic (short-termist). So they may undervalue the long-term benefits of having a well funded pension, such as financial security in retirement.

In other words, consumers perceive the marginal private benefit of pension contributions as lower than the actual marginal private benefit.

People may also have imperfect information about the benefits of having a pension.

Also there can be many options for pension providers for consumers to choose from. This can be confusing for consumers and result in information overload. Consumers when faced with confusing choices, may be less likely to make any choice.

The UK Government changed employer pension schemes to be opt-out for employees (“automatic enrolment”), rather than opt-in. This makes use of a consumer status quo or default bias – consumers are more likely to stick to a default option, than to change to the non-default option.

Such a nudge increases demand for pensions.

Also it has been shown that if firms reduce the number of available pension options, then signing up to a pension is more likely. This increases pension demand further. Overall pension demand shifts right from D to D1, increasing pension contributions to the socially optimal level at q1, where actual MPB = MPC. This eliminates market failure and improves social welfare.

Restricting choice

Mandated choice and nudges generally can be seen as violating individual freedoms. Consumers may be making choices subject to manipulation without their knowledge, which risks being used to lower consumer surplus. Indeed consumers may know better than governments about the choices that maximise utility.

Consumers could hence see such nudges as paternalistic – the government oversteps in instances where the consumer knows better.

A nudge in the Netherlands backfired, when organ donation was changed from an opt-in to an opt-out scheme. In a subsequent donor drive, the percentage registering as non-donors increased relative to before the nudge.

This would reduce the amount of organs available for transplants, further worsening social welfare. So nudges can lead to unintended consequences, such as rebellion.

Other possible points

- Other examples of nudges and choice architecture, including restricted choice.

- Low cost of nudges.

- One key advantage of nudges is they can be tested in experiments in multiple different countries and settings. Generating “repeatability” allows policymakers to figure out which nudges work well and how best to write. This means nudges are likely to become more effective.

- May preserve freedom of choice, compared to a complete ban or harsh regulation.

- Policies may have different effects on different groups.

- Nudges / choice architecture could be manipulated by governments or firms, such that consumers act against their best interests.

- Under the choice architecture or nudge policies, decisions may not reflect underlying consumer preferences. So such policies can lead to lower consumer surplus. Consumers may be rational in not taking up pensions enough or not eating certain foods, for example.

- The Government may use nudges as a substitute for taxes, subsidies or regulation. The nudges may only have a small effect. But a larger effect from traditional economic policy may be required.

Evaluation points for behavioural economics policies

The success of nudge style policies depends on the:

- Level of information the government has. The government may misidentify the socially optimal level of healthy food, for example. If the government underestimates the socially optimal level of healthy food, it may not give strong enough nudges, so demand may not increase enough to meet socially optimal healthy food consumption. Moreover if the government underestimates the socially optimal level of healthy food, it may rely too heavily on nudges, which may have little power compared to policies like taxes, subsidies or regulation which may be required to bring about the socially optimal outcome. So nudges are only useful depending on the information level of the government.

- Coverage of the scheme. The automatic enrolment for pensions in the UK does not cover everyone in particular the self-employed, and people can still choose to opt out. Self-employment is increasing as a share of the total workforce in the UK with the rise of gig economy work and zero hours contracts. Because this work is more likely to be insecure with varying hours and wages, there is even greater need for pensions among this group to ensure a stable retirement. So changing choice architecture can improve welfare but is not sufficient – other policies may be needed.

- Type of nudge policy used. Changes to choice architecture where consumers can realise they are being manipulated, may be more likely to generate protest and backfiring. Small changes to the framing of choice, without any legal consequences, are likely to preserve the ability of consumers to make choices to a greater degree. This reduces the likelihood of rebellion against the intended direction of the policy, making the policy more likely to be successful. So while nudges can have unintended consequences, the nature and the language of the nudge can mitigate these concerns.

- The level of trust and transparency between governments and consumers. Nudges, particularly where there are significant changes to the choice architecture can also threaten freedoms and appear paternalistic, and could be manipulated against consumer interests. Trust and transparency between governments and consumers will help make for more successful nudges in line with what is best for consumers, without overstepping.

Related posts

To view other A-level Economics resources, check out these links below:

Sources: Behavioural Insights Team, miscellaneous others.

For more information about the state of nudges, I recommend reading this report here.

Latest posts

- 3.5.3 Wage determination in labour markets – Edexcel A notes

- 2024 Paper 1 Edexcel Economics A Full Model Answers

- All key diagrams for Themes 1 and 3 | Edexcel Economics A

- 3.3.4 Normal profits, supernormal profits and losses – notes for Edexcel Economics A

- How to read academic papers for economics – a guide